- >

- Business loans>

- 50+ UK Business Loan Statistics 2023 | money.co.uk

50+ UK Business Loan Statistics 2023

This page includes relevant UK business loan statistics for 2023, such as borrowing data, average costs, approval rates, and the main reasons UK businesses take out loans.

For generations, business loans have been used by companies of all sizes to add an influx of cash in times of need. From start-up companies to established brands, business owners often make applying for a business loan their first port of call when seeking financial support to grow their company or overcome short-term issues.

With recent challenges, such as COVID-19 and the cost-of-living crisis, many businesses have sought external finance to cope with the rising cost of daily operations.

Our research has gathered over 50 of the most prominent UK business lending statistics for 2023, including information on average borrowing, approval rates and the size of the UK commercial lending market.

Top seven UK business loans statistics 2023

Gross lending for UK businesses is expected to hit £496 billion in 2023.

The overall value of UK SME bank loans reached £65.1 billion in 2022 – up 12.8% from 2021.

London topped UK mainland regions with the highest rate of SME borrowing for loans and overdrafts (£22.8 billion) in the second half of 2022.

The median average value of SME loans was £14,000 in 2022 – a 40% rise since 2021.

More than a third (36%) of SMEs used external finance in 2022, borrowing more than £25,000 on average.

More than two-thirds (69%) of SMEs claimed their reason for requiring external finance was “cash flow related”.

More money was borrowed in the South East per start-up loan than in any other UK region, with an average amount of £10,179.

Bank of England business loan interest rates

The Bank of England’s (BoE) base rate is the interest rate set by the UK’s central bank. It changes regularly in response to the country’s current economic state. Commercial banks and lenders use the BoE rate as a guide when setting interest rates on business loans and other forms of borrowing.

On 3 August 2023, the BoE’s base rate was set to 5.25% – the highest rate since 2008. The base rate has risen sharply since 2021 in an attempt to reduce inflation. It had previously fallen to a historic low of 0.1% in 2020 during the COVID-19 pandemic.

In June 2023, the annual growth rate of borrowing by small-to-medium enterprises (SMEs) was down 4.2% on the previous June – up from -4.3% in May 2023.

How much is the UK business loans market worth?

The latest UK business lending statistics found that gross lending for UK businesses is projected to reach £496 billion in 2023 – a 4% rise from 2022 (£477 billion) – the highest figure recorded since 2011.

A breakdown of the total value of UK business lending by year from 2013-2023

UK business lending has increased significantly since 2016, when it stood at just over £389 billion. By 2020, this figure had climbed by 15% to £447.3 billion before falling slightly (-2%) in 2021. By 2022, it had risen again by 4% compared to the previous year.

If the projections for 2023 prove correct, business lending will have grown by more than a quarter (27%) in the seven years since 2016.

How much are UK SMEs borrowing?

Recent small business lending statistics found that the total value of SME bank loans in the UK reached £65.1 billion in 2022. This marks a 12.8% increase from 2021 (£57.7 billion) and is the second-highest figure on record.

A breakdown of the gross value of bank loans to UK SMEs between 2017 and 2022

SME bank lending remained steady between 2017 and 2019, going from £56 billion to £58 billion, respectively, before accelerating to over £100 billion (+84%) during the COVID-19 pandemic in 2020.

Though a 44% drop between 2020 and 2021 brought the numbers back to their pre-pandemic rates, the 2022 figures mark only the second time that the gross value of SME bank loans has exceeded £60 billion.

Despite the significant rise between 2021 and 2022, the latest figure of £65.1 billion remains 38% lower than the industry’s 2020 peak of £104.9 billion.

Which UK region has the most SME borrowing?

According to a UK Finance report, London had the highest level of SME borrowing in mainland Britain in the second half of 2022. The outstanding value of the capital’s business loans and overdrafts totalled £22.8 billion – 71% more than any other region and nearly a quarter (23%) of mainland Britain’s total lending for the second half of 2022.

A regional breakdown of the total outstanding value of business loans and overdrafts for Great Britain (GB) SMEs in the second half of 2022

The latest business lending stats show that southern regions dominate SME borrowing. The South East (£13.3 billion) and South West (£11 billion) are the only regions besides London with outstanding loans and overdrafts of more than £10 billion.

The North East was the region with the lowest level of borrowing in the second half of 2022, with its total outstanding value of £3.2 billion – around 86% lower than that of London and 76% less than the South East.

Scotland had the highest SME borrowing in the second half of 2022 after England, with £8.1 billion in loans and overdrafts. This is around 88% higher than similar borrowing in Wales, which stands at £4.3 billion.

How much are SMEs relying on invoice finance and asset-based lending?

The latest UK business loan stats found a considerable increase in invoice finance and asset-based lending for SMEs between 2021 and 2023. During the first two quarters of 2021, the total value of invoice finance ranged between £1 billion and £1.5 billion.

Asset-based lending first exceeded £1.5 billion in the third quarter of 2021 before climbing above £2 billion in the second quarter of 2022. Things have remained relatively stable since then, with the total value of invoice finance and asset-based lending standing at approximately £2.1 billion during the first quarter of 2023.

How much do SMEs borrow on average?

An SME report from the British Business Bank found an increase in the average business loan size for SMEs between 2021 and 2022. The median average value of SME loans in 2022 was £14,000 – a 40% rise from the year before when the median value was £10,000.

A breakdown of the median value of business loans by type of business in 2021 and 2022

| Type of business | Median amount borrowed in 2021 | Median amount borrowed in 2022 |

|---|---|---|

| All SMEs | £10,000 | £14,000 |

| SMEs with no employees | £10,000 | £10,000 |

| SMEs with employees | £25,000 | £25,000 |

(Source: British Business Bank)

These increases aren’t as obvious when breaking down SMEs into various categories. The median average value of loans for SMEs with no employees has remained consistent across both years (£10,000), as have the figures for SMEs with employees (£25,000).

How many UK SMEs require external finance?

The latest UK business lending statistics found that 36% of SMEs used external finance in 2022, with one in three borrowing more than £25,000. This represented a decrease of 7% from 2021 when the number of SMEs using finance for their business stood at 43%.

There was a significant difference between the size of SMEs and the typical business loan amount between 2021 and 2022. Less than a quarter (23%) of businesses with zero employees borrowed more than £25,000, compared to 84% of those with 50-249 employees.

Almost half (48%) of SMEs met the definition of a permanent non-borrower: an SME that is not currently borrowing and is considered unlikely to do so.

What are the most popular types of external finance in the UK?

Bank overdrafts, government grants and business credit cards were the most popular forms of external finance used between 2019 and 2022. Around 12% of UK SMEs used at least one of these borrowing options in the three years leading up to 2022.

Although government and local grants remain among the most common forms of external finance, the number of SMEs seeking these types of finance has declined dramatically since the previous year, when just over a quarter (26%) applied for a government or local grant.

Conversely, the percentage of SMEs seeking overdrafts remained identical between 2021 and 2022, while the number applying for credit cards dropped by just 1%.

A breakdown of the percentage of SMEs who applied for various forms of external finance in 2021 and 2022

Bank loans and private lending experienced the biggest spikes in demand between 2021 and 2022, with both rising 3% to 10% and 7%, respectively. The only other form of finance that increased in demand during this period was loans from a director, individual or other organisation, which increased from 10% to 11%.

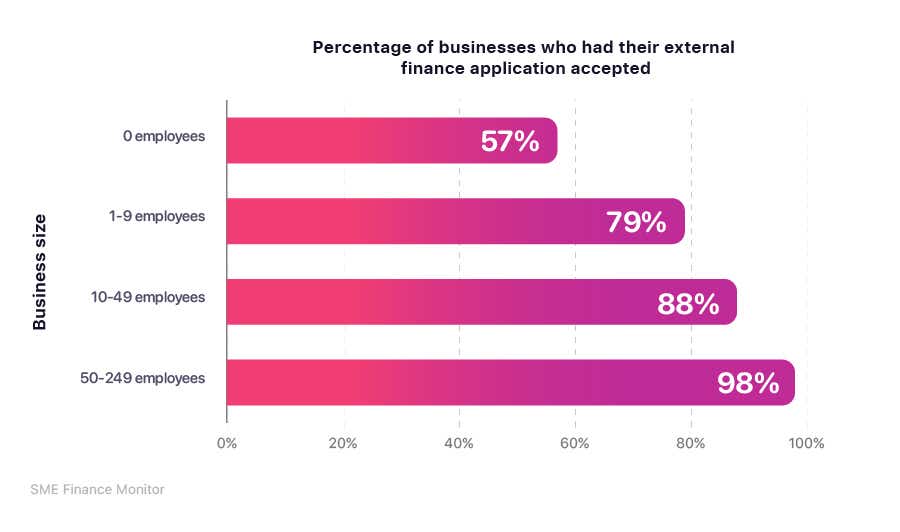

How many UK SMEs are approved for business loans?

The latest UK business lending statistics found a direct correlation between SME size and successful loan applications. Companies with zero employees experienced the lowest success rates, with just over half (57%) of their applications for external finance being accepted.

A breakdown of the percentage of SMEs who had their external finance application by business size

The most dramatic rise occurred between SMEs with no employees and those with one to nine employees, with acceptance rates accelerating from 57% to 79% (+22%). This is followed by another sharp rise of 9% for SMEs with 10-49 employees.

By the time we reach the largest business category (50-249 employees), the application success rate for external finance stands at 98%. This means that 49 out of every 50 applications from the UK’s biggest SMEs are likely to succeed.

What are the main reasons SMEs take out loans?

Business lending statistics from SME Finance Monitor for the fourth quarter of 2022 show that “cash flow” was the most common reason for borrowing money, with more than two-thirds (69%) of SMEs giving this as their reason for applying. This was followed by “working capital”, which was cited by nearly half (49%) of SMEs.

A breakdown of why funding was required by UK SMEs in Q4 2022

| Why was funding required? | All SMEs | 0 employees | 1-9 employees | 10-49 employees | 50-249 employees |

|---|---|---|---|---|---|

| Cash flow related | 69% | 70% | 64% | 64% | 62% |

| Working capital to help with cash flow | 49% | 50% | 44% | 49% | 55% |

| To cover a short-term funding gap | 36% | 39% | 29% | 21% | 9% |

| To cope with the impact of the pandemic | 20% | 22% | 16% | 13% | 1% |

| To help through trading difficulties | 24% | 26% | 18% | 11% | 2% |

(Source: SME Finance Monitor)

The number of SMEs borrowing to cover a short-term funding gap decreased dramatically in 2022 as the size of the business increased. Less than one in 10 (9%) of SMEs with 50-249 employees sought funding for this purpose, compared to 39% of businesses with no employees.

Similarly, one in five (20%) of SMEs sought finance to cope with the impact of the COVID-19 pandemic. Yet, only 1% of the largest companies (50-249 employees) cited this as a determining factor, compared to more than a fifth (22%) of zero-employee businesses.

Unsure whether or not to seek external finance? Our comprehensive guide will help you decide whether borrowing could boost your business.

A breakdown of why funding was required by UK SMEs in 2022 by year

| Why was funding required? | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|

| Business development related | 58% | 24% | 24% | 37% |

| Invest in a new plant, machinery, etc. | 25% | 9% | 11% | 14% |

| To fund expansion in the UK | 20% | 11% | 9% | 19% |

| A new business opportunity | 13% | 4% | 5% | 11% |

| To fund research and development | N/A | N/A | N/A | N/A |

| To fund new premises | 7% | 1% | 2% | 3% |

| To take on staff | 5% | 2% | 1% | 4% |

| To fund expansion overseas | 3% | 1% | 1% | 3% |

(Source: SME Finance Monitor)

The SME Finance Monitor report found that more than a third (37%) of SMEs stated that “business development” was their primary reason for requesting additional funding in 2022 – 18% more than any other purpose. This represented a 13% rise since 2021, when less than a quarter (24%) gave this as their reason for getting a business loan.

A breakdown of why funding was required by UK SMEs in 2022 by business size

| Why was funding required? | All SMEs | 0 employees | 1-9 employees | 10-49 employees | 50-249 employees |

|---|---|---|---|---|---|

| Business development related | 37% | 36% | 40% | 39% | 38% |

| Invest in a new plant, machinery, etc. | 14% | 14% | 16% | 16% | 23% |

| To fund expansion in the UK | 19% | 20% | 16% | 13% | 8% |

| A new business opportunity | 11% | 11% | 11% | 7% | 12% |

| To fund research and development | 5% | 5% | 4% | 2% | - |

| To fund new premises | 3% | 2% | 5% | 5% | - |

| To take on staff | 4% | 4% | 5% | 7% | 3% |

| To fund expansion overseas | N/A | N/A | N/A | 1% | 5% |

(Source: SME Finance Monitor)

Around one in five (19%) of SMEs sought finance to “fund expansion in the UK”, a rise of 10% from 2021, while 14% of all SMEs sought finance to “fund new plant machinery”, a figure that rose to almost a quarter (23%) for SMEs with 50-249 employees.

Want advice on how to get a business loan? Visit our comprehensive business loans guides for expert tips on this and more.

UK business start-up loan statistics

The latest UK business statistics reveal that the total number of UK start-up loans exceeded 100,000 in February 2023. A press release at the time of the landmark loan also announced that since its introduction in 2021, the government-backed scheme has provided more than £941 million in funding to those starting a business.

Of those loans, two in five (40%) went to women, and one in five (20%) to people from Black, Asian, or other ethnic minority backgrounds. Young entrepreneurs also benefited, with 14% of start-up loans going to people aged between 18 and 24.

Which region borrows the most in start-up loans?

Newly launched businesses in the South East borrow the most on average, with the average start-up loan in the area standing at £10,179. The region’s overall value of start-up loans is just under £102 million. According to business lending statistics, that is the third-highest figure behind London and the North West.

Although London’s total loan value of £192 million is substantially higher than the South East, it’s average loan value £9,204 is 9.5% lower. This is because more than twice as many start-up loans were issued in London compared to the South East (20,937 vs 9,997).

A regional breakdown of the total number of UK start-up loans and their average value

Aside from the South East, Wales was the only other region with an average loan value exceeding £10,000. Its figure of £10,012 indicates that Welsh start-up companies’ average loans are around 12% more than those in Scotland and almost 16% more than those in Northern Ireland.

Northern Ireland’s average start-up loan was the lowest of any UK region, at £8,661. This figure was around 3% less than the next lowest region (Scotland) and 15% less than the South East. Northern Ireland also recorded the lowest overall loan value, with around £13.3 million (93% less than London’s).

Business loans FAQs

What is the average interest rate on a business loan in the UK?

According to Experian, interest rates on a UK business bank loan vary between 2% and 13%. However, interest rates on a business loan can vary based on numerous factors, including the loan’s type and value, company size and the business or individual’s credit history.

Do business loans hurt your credit?

Taking out a business loan shouldn’t harm your personal credit rating. However, missing payments for your business loan could impact your personal credit rating if you personally guaranteed your business account in any way.

What is the best way to get a business loan?

There are numerous ways to enquire about taking out a business loan, from visiting a bank branch in person to applying online. Using a reputable price comparison site, like Money.co.uk, allows you to compare the best rates on loans from leading banks and financial organisations to ensure you get the right deal for your company.

Do most small businesses start with a loan?

New businesses often need to borrow money to fund equipment, supplies, advertising and payroll needs. This can be in the form of a start-up loan, standard business loan or other form of external finance.

Are business bank loans secured or unsecured?

Business loans can be taken out as secured loans or unsecured loans.

You can usually take out an unsecured loan for smaller amounts. In contrast, more significant sums tend to require secured business loans, with an asset acting as security for the lender.

Am I eligible for a business loan?

The eligibility for business loans can vary between issuers. However, all reputable business loan providers want you to:

Be aged 18 or over

Pass credit checks and demonstrate you can afford loan repayments

Prove that you own a business or plan to start one

Tell them how you plan to use the loan

Can I get an overdraft on my business account?

Yes. Like personal accounts, most business bank accounts will allow you to set up an overdraft facility provided you meet the criteria. These can vary from bank to bank but are typically influenced by your current finances and credit or payment history.

Business loans glossary

Glossary of terms

Asset-based lending

Asset-based lending is when a business uses an asset, such as a building, premises or inventory, as collateral in order to acquire finance.

Government grant

A government grant is a sum of money awarded to your business by the UK government. You do not have to pay back these sums. Grants are typically awarded to companies to fund specific developments.

Gross lending

Gross lending refers to the total amount of loans a bank or institution advances over a given period. It excludes repayments and other adjustments.

Hire purchase

Hire purchase is where a business or individual acquires an item without paying the full purchase price at the outset. Instead, they make pre-arranged payments according to an established schedule.

Invoice finance

Invoice finance is when a business uses unpaid customer invoices as collateral to acquire funding from a lender.

Overdrafts

An overdraft is a form of debt that allows you to take out more money than you have in your bank account. You are said to be overdrawn if your balance falls below £0. There is generally a limit to your overdraft and a charge for being overdrawn.

Start-up loans

Start-up loans are supplied as part of a government-backed scheme in which prospective new businesses (or businesses that have been trading for less than 36 months) can receive funding to help with costs like equipment, stock, premises, marketing and promotional expenses.

Sources

https://www.bankofengland.co.uk/statistics/visual-summaries/businesses-finance-raised

https://www.bankofengland.co.uk/monetary-policy/the-interest-rate-bank-rate

https://www.ibisworld.com/uk/bed/business-lending/44246/

https://www.ey.com/en_uk/news/2023/02/uk-business-lending-to-contract-sharply-this-year

https://www.ukfinance.org.uk/data-and-research/data/sme-lending-within-uk-postcodes

https://www.british-business-bank.co.uk/wp-content/uploads/2023/02/J0189_BBB_SBFM_Report_2023_AW.pdf

https://www.bva-bdrc.com/wp-content/uploads/2023/08/BVABDRC_SME_FM_Q4_2022.pdf

About Cameron Jaques

Cameron has worked within the SME industry for over five years, looking after all our SME commercial relations for money.co.uk including Business Loans, Business Current Accounts, and Business Credit Cards.