- >

- Business loans>

- 50+ UK Business Loan Statistics 2025 | money.co.uk

50+ UK Business Loan Statistics 2025

This page includes relevant UK business loan statistics, such as the evolution of the business loans market, how UK SME lending stats have changed over time, and what the average business loan looks like in 2025.

What is a business loan?

A business loan is a specified sum of money that you agree to pay back (with interest) over a defined period and must be used for business purposes.

From start-up companies to established brands, business owners often apply for a business loan as their first port of call when seeking financial support to grow their company or overcome short-term issues. For generations, business loans have been used by companies of all sizes to inject cash in times of need.

With recent challenges, such as the COVID-19 pandemic and a cost-of-living crisis, many businesses have sought external finance to help cope with the rising cost of daily operations.

Our report has compiled the most prominent business loan statistics, including how UK small business lending statistics have evolved, what the average business loan looks like in 2025, and the latest facts surrounding business loan interest rates.

Top 10 must-know UK business loan statistics 2025

The UK business loans market is worth a reported £485.9 billion.

The total value of annual UK SME borrowing is estimated to be around £62.1 billion.

Just under two-fifths of UK SMEs opt for a business loan between £5,000 and £24,999.

As of Q2 2025, almost £2.26 billion of business lending came from loans.

Approximately three in five UK SMEs have their business loan application approved.

The most common reason for having a business loan application rejected is due to the company's current business performance (26% of cases).

The number of start-up loans across the UK increased by a fifth between 2020 and 2025, to 120,221.

Newly-launched businesses in the South East tend to borrow the most across all UK regions, with an average start-up loan of £10,884.

Approximately two in five UK SMEs require external finance.

Credit cards are the most common form of external finance, used by almost one in six UK SMEs.

How much is the UK business loans market worth?

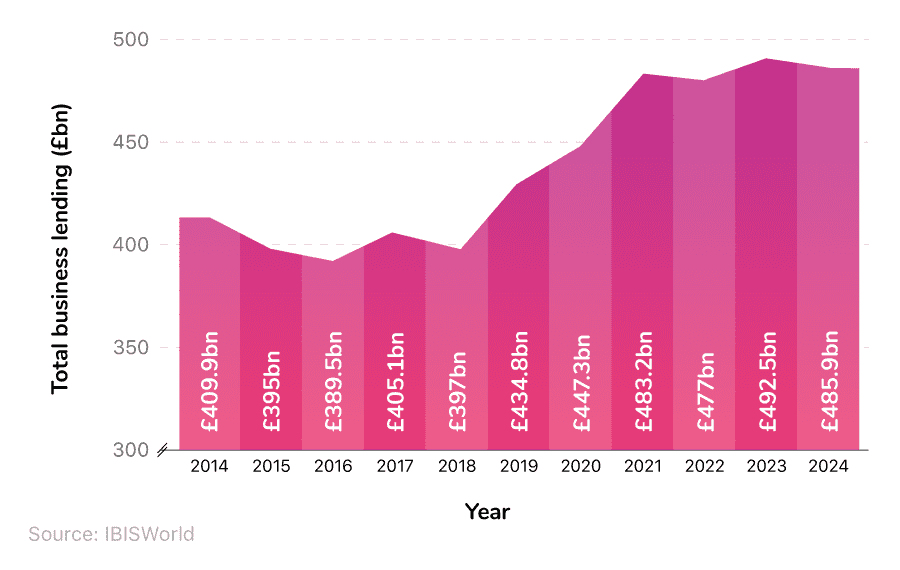

The latest UK business lending statistics indicate the business loans market was valued at £485.9 billion in 2024, a 1.3% decrease from 2023.

UK gross business lending statistics over time

The total value of gross business lending fluctuated between 2016 and 2024, from a low of £389.5 billion in 2016 up to a peak of £492.5 billion in 2023 (a rise of 26.4% in the space of seven years).

The total value of UK business lending by year

Between 2014 and 2016, the amount of lending to UK businesses experienced a gradual year-on-year decrease of almost 5%.

However, from 2018 onwards, this figure has been on a steady upward trajectory, with a slight dip in 2022 (-1.3% compared to the previous year).

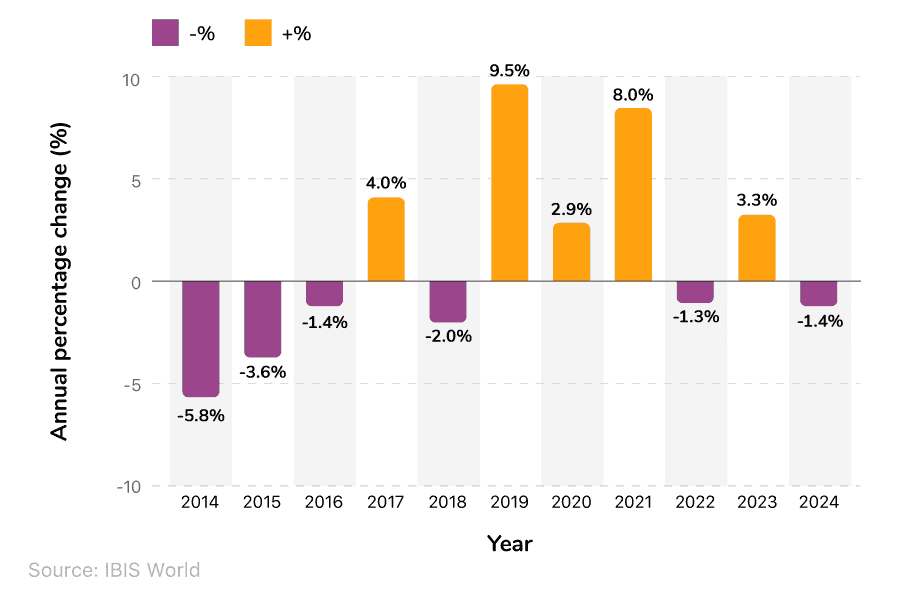

Annual percentage change in gross lending statistics to UK businesses over time

As of 2024, the annual percentage change in the gross lending to UK businesses stood at -1.4% compared to 2023.

In the previous decade, the largest change was between 2018 and 2019, when the UK business loans market grew by approximately 9.5% in 12 months.

Contrastingly, the biggest year-on-year decrease in UK business lending occurred in 2014, when the estimated value declined by 5.8% from the previous year.

UK business lending statistics

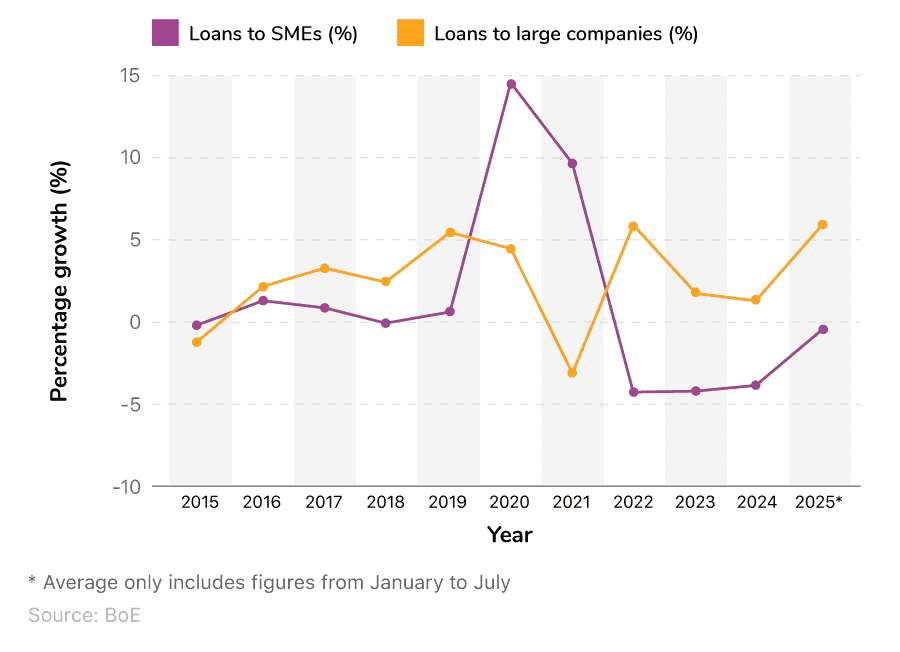

According to the latest business lending statistics from the Bank of England (BoE), loans to large companies in 2025 grew by 6.24% compared to the previous year (the largest year-on-year increase in the past decade).

By contrast, the average annual growth rate for lending to SMEs in 2024 was -0.74%, compared to the 2023 figures.

UK SME lending statistics over time vs. large businesses

The growth rate for UK SME lending has been in a year-on-year decline since 2020, when it reached a peak of 14.73%. However, since 2023, the figures have started to increase slowly, yet they still remain negative.

Average annual growth of lending to UK SMEs and large businesses over time

Conversely, the UK's average annual growth rate of loans to large companies fluctuated from 2015 to 2025, ranging from a low of -3.68% between 2020 and 2021 to a high of +6.17% in 2025, compared to the lending figures for 2024.

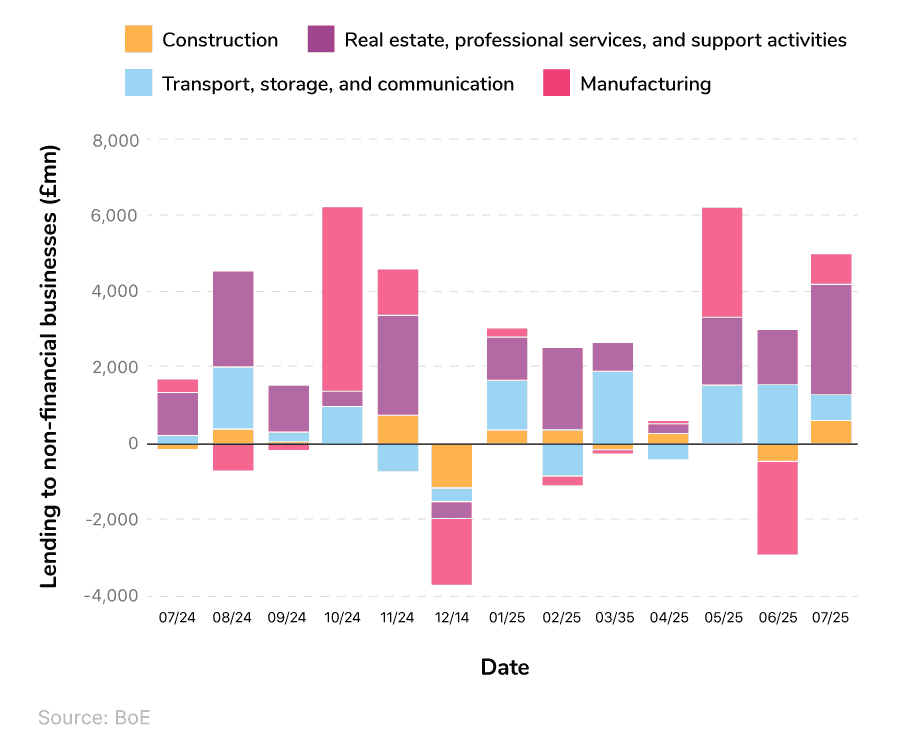

UK business lending statistics over time, based on sector

Lending to most non-financial industries fluctuated greatly between July 2024 and July 2025.

The majority of months during this time witnessed some degree of positive lending, except December 2024, which cumulatively saw a drop of almost £3.68 billion across all sectors.

UK business lending statistics to non-financial businesses over time

The real estate, professional services, and support activities industry experienced the largest amount of business lending throughout 2024 and 2025, with December 2024 registering the only negative figure during this period.

Net business lending for this sector totalled nearly £17.8 billion between July 2024 and July 2025. This was more than double the next highest category (transport, storage, and communications) at £7.8 billion and approximately 3.5 times more than manufacturing (at almost £5.0 billion).

Conversely, the construction industry experienced some of the largest fluctuations in the value of its monthly business lending during this period. Ranging from a peak of £759 million in November 2024 to a low of -£1.1 billion the following month, this sector experienced net business lending of just over £1 billion between July 2024 and July 2025.

UK business loan interest rate statistics

The BoE’s base rate is the interest rate set by the UK’s central bank. It changes regularly in response to the country’s current economic state. Commercial banks and lenders use the BoE rate as a guide when setting interest rates on business loans and other forms of borrowing.

On 3 August 2023, the BoE’s base rate was set to 5.25%—the highest rate since 2008. It rose sharply after 2021 in an attempt to reduce inflation, having previously fallen to a historic low of 0.1% in 2020 during the COVID-19 pandemic.

As of September 2025, the BoE base rate stood at 4%.

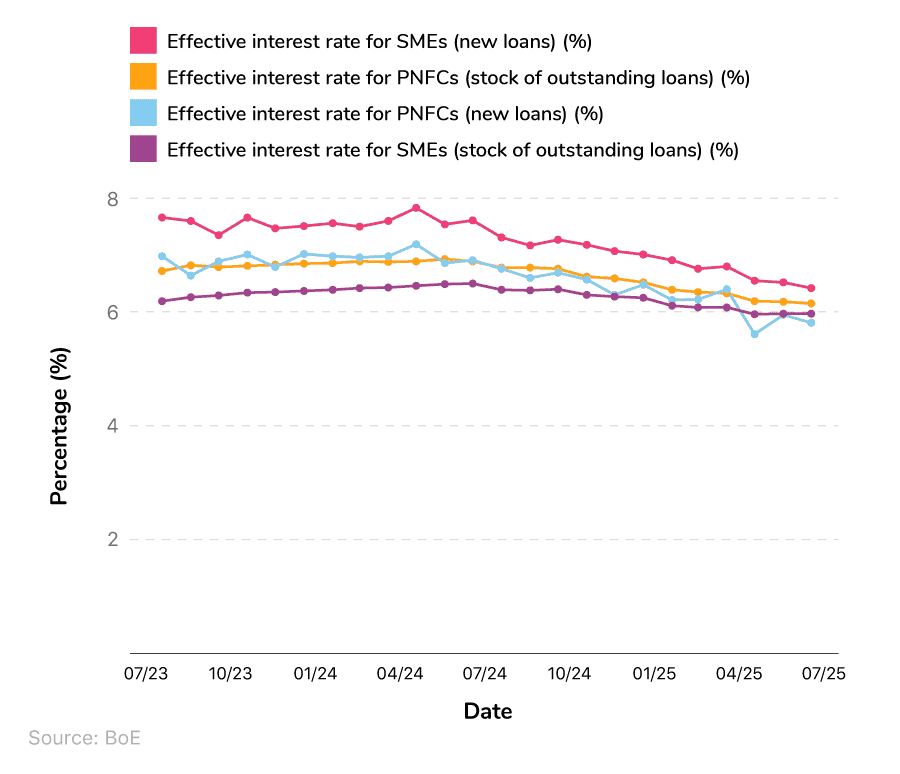

Effective business loan interest rates in the UK

As of June 2025, the effective business loan interest rate for Private Non-Financial Corporations (PNFCs) on the stock of outstanding loans stood at 6.17%. This represented a decrease of more than 10% compared to the previous 12 months.

Comparative figures show a fall of almost 13.3% over the same period (6.85% vs. 5.94%, respectively).

Effective business loan interest rates for UK PNFCs and SMEs over time

Effective small business loan interest rates for the stock of outstanding loans fluctuated between August 2023 and June 2025, reaching a high of 6.49% in July 2024.

From here, there was a month-on-month decrease in the average business loan rate for SMEs to a low of 5.95% in May 2025. This represents an 8.3% decline over the past 10 months.

Conversely, the effective interest rate for new loans to SMEs generally remained above 7% between August 2023 and January 2025, before falling month-on-month in Q1 and Q2 of 2025 to 6.51% in June.

UK SME borrowing statistics

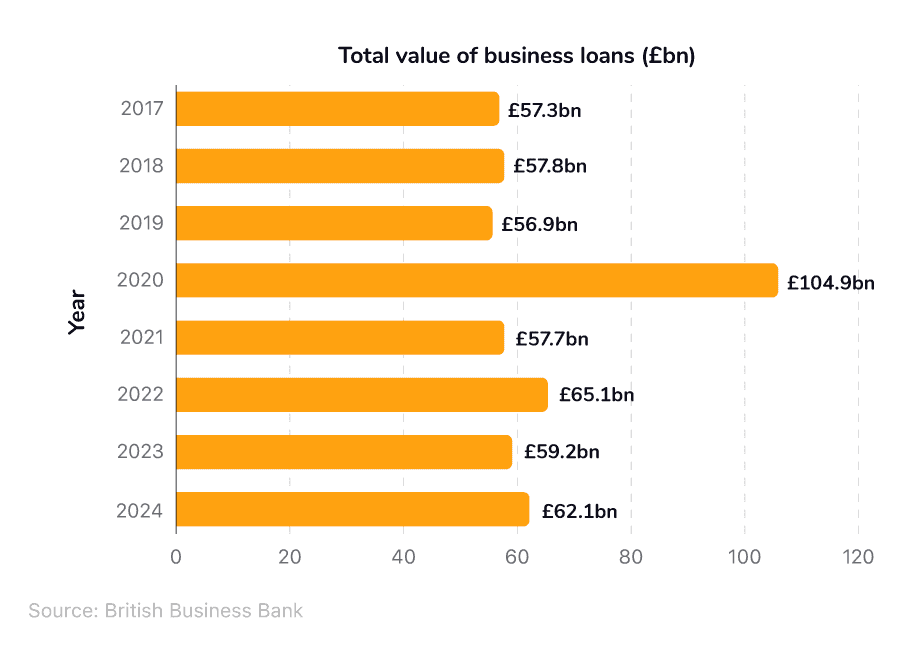

How much are UK SMEs borrowing?

Recent small business lending statistics indicate that the total value of SME bank loans in the UK reached £62.1 billion as of 2024. This marks a 4.9% increase from 2023, when the figure stood at £59.2 billion.

The value of business loans to UK SMEs over time

SME bank lending remained steady between 2017 and 2019, falling from £57.3 billion to £56.9 billion, respectively. This accelerated by +84% to almost £105 billion during the COVID-19 pandemic in 2020.

Though a 44% drop between 2020 and 2021 brought the numbers back to their pre-pandemic rates, the 2024 figure marks only the third time that the gross value of SME bank loans has exceeded £60 billion in recent years.

How much do SMEs borrow on average?

According to the latest small business loan statistics, UK SMEs invested £12.31 billion in 2024. This was less than half the respective figure compared to large businesses (i.e. those with 250 or more employees).

The average amount of borrowing by different-sized UK businesses

| Business size | Gross Value Added (GVA) (£bn) | Median investment (as a % of GVA) | Total investment (approx. GVA x median) (£bn) |

|---|---|---|---|

| 1 to 9 | 263.41 | 1.14% | 3.69 |

| 10 to 49 | 199.52 | 1.44% | 2.87 |

| 50 to 249 | 219.56 | 2.62% | 5.75 |

| 250 and over | 630.38 | 4.40% | 27.74 |

(Source: British Business Bank)

Of the total amount invested in 2024 by UK SMEs, almost 47% came from those with 50 to 249 workers.

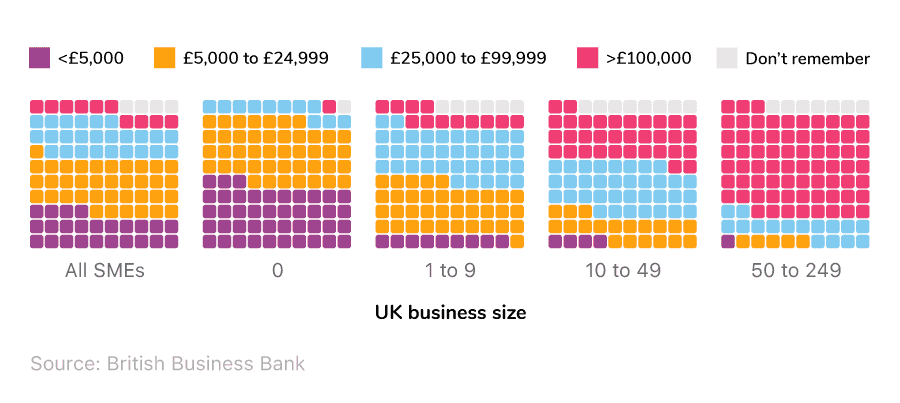

Average business loan amount by different-sized UK businesses

Business loan statistics from the BVA BDRC reveal that just under two-fifths of UK SMEs took out a loan in 2024, with the amount ranging between £5,000 and £24,999. This was followed by a quarter who either opted for a loan between £25,000 and £99,999 or one for less than £5,000. This meant that, on average, just one in 10 SMEs borrowed £100,000 or more per year.

As business size increases, so does the rate of borrowing at the higher end. For example, seven in 10 companies with 50 to 249 employees took out a loan worth £100,000 or more in 2024, compared to double the proportion of businesses with a workforce between 10 and 49 employees.

Just over two-fifths of UK micro-businesses (i.e., those with no employees) took out a loan in 2024 that was either less than £5,000 or between £5,000 and £24,999, compared to one in 100 who opted for a loan of £100,000 or higher.

Incidentally, one in 25 companies surveyed by BVA BDRC could not remember how much their loan was for the year.

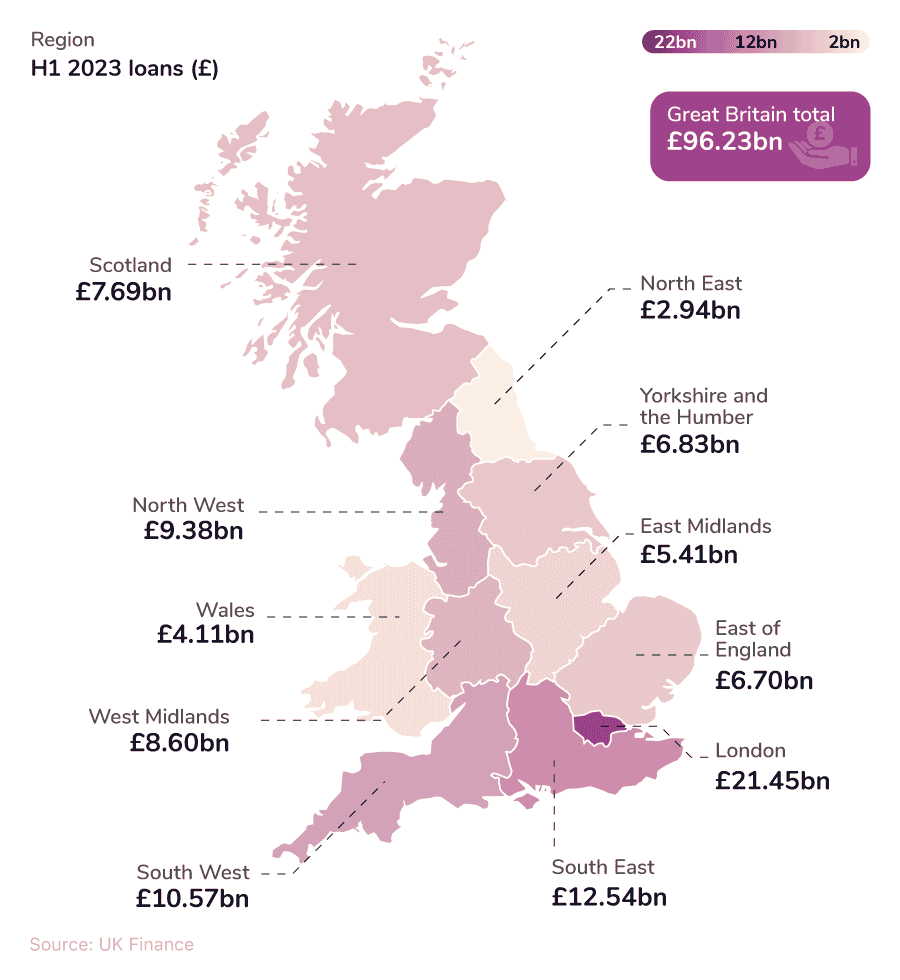

Which UK region has the most SME borrowing?

According to a UK Finance report, London had the highest level of SME borrowing in mainland Britain throughout the first half of 2023. The outstanding value of the capital’s business loans and overdrafts totalled £21.45 billion in H1 2023, representing 22% of mainland Britain’s total lending.

Total outstanding value of business loans and overdrafts for Great Britain (GB) SMEs as of H1 2023

Business lending stats show that southern regions tend to dominate SME borrowing across the UK. The South East (£12.54 billion) and South West (£10.57 billion) are the only regions outside of London with outstanding loans and overdrafts of over £10 billion.

The North East was the region with the lowest level of borrowing in the first half of 2023, with a total outstanding value of £2.94 billion. The North East also showed the biggest decrease in outstanding value, dropping by 7.62% between H2 2022 and H1 2023.

All UK regions saw a decrease in the total outstanding value of business loans and overdrafts between the end of 2022 and the beginning of 2023. The South West had the smallest decline at 4%, while the average for Great Britain was 5.26%.

UK business lending statistics over time vs. other sources of finance

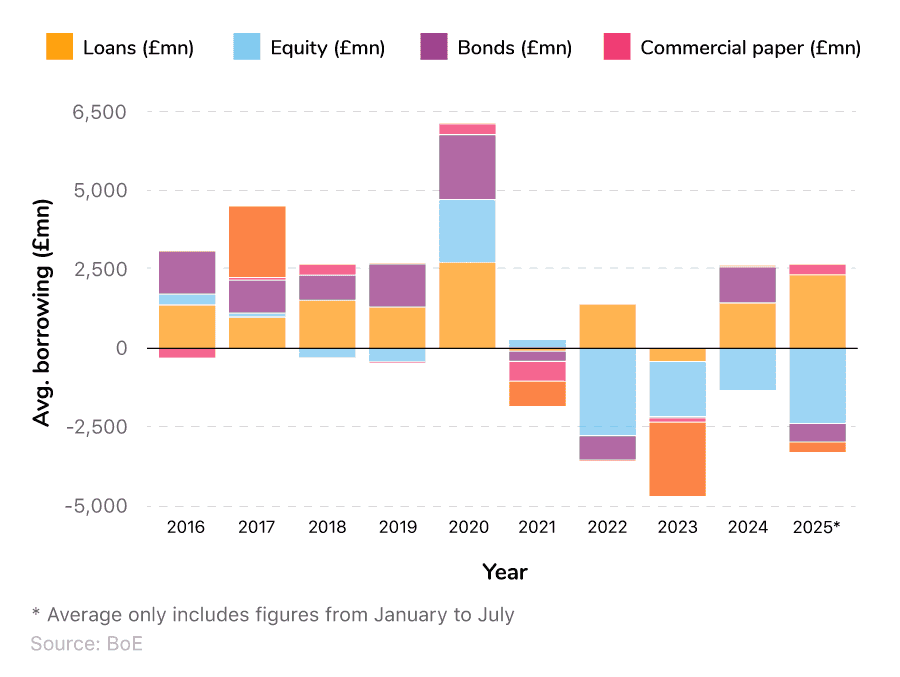

In the year to July 2025, net business borrowing by UK businesses across all sources stood at -£312 million. However, this overall figure doesn’t tell the whole story.

During the first six months of the year:

£2.33 billion of business lending from loans was offset by a similar amount from equity sources.

Approximately £315 million was borrowed by UK businesses from commercial papers, compared to -£588 million from bonds.

Average business borrowing from UK banks, building societies, and capital markets over time

Between 2016 and 2025, the average annual value of loan borrowing by UK businesses fluctuated, but largely stayed in the positive (with the exceptions of 2021 and 2023).

During this time, it ranged from a low of -£416 million in 2023 up to a peak of almost £2.73 billion in 2020 (the largest difference among all sources of borrowing at £3.15 billion).

By contrast:

Equity borrowing by UK businesses dropped to a low of around -£2.76 billion in 2022, yet only reached a high of £350 million in 2016 (a difference of £3.11 billion).

The value of borrowing from bonds was -£588 million in 2025, yet peaked at roughly £2.06 billion in 2020 (a difference of almost £2.65 billion)

Borrowing by UK businesses from commercial papers ranged from -£629 million in 2021 up to £315 million in 2025 (a difference of £944 million).

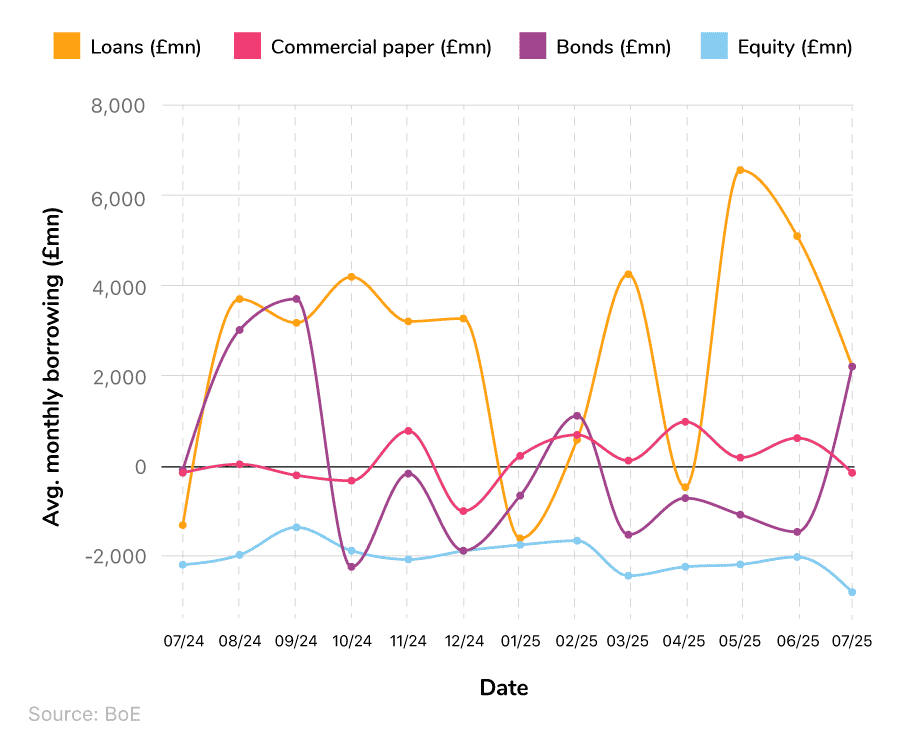

Monthly average business borrowing from UK banks, building societies, and capital markets

As of July 2025, the monthly average for businesses borrowing via loans stood at just over £2.16 billion. This indicated a drop of around two-thirds from May, which recorded the highest value for loan borrowing over the last year.

Just three months in the previous 12 recorded a negative amount of loan borrowing by UK businesses, reaching a low of almost £1.7 billion in January 2025.

Contrastingly:

Equity borrowing by UK businesses remained negative over the last 12 months, ranging from -£1.15 billion in June 2024 down to -£3.38 billion in April 2025 (a difference of £2.23 billion).

The value of borrowing from bonds during this time reached a peak of roughly £3.67 billion in September 2024, before falling to a low of -£2.30 billion the following month. This resulted in a difference of just over £5.96 billion (the largest range across all sources of business borrowing for the year).

UK business borrowing from commercial papers had the smallest difference across all four sources, ranging from around -£1.06 billion in December 2024 up to a peak of £933 million in April 2025—a difference of approximately £1.99 billion.

UK business loan approval statistics

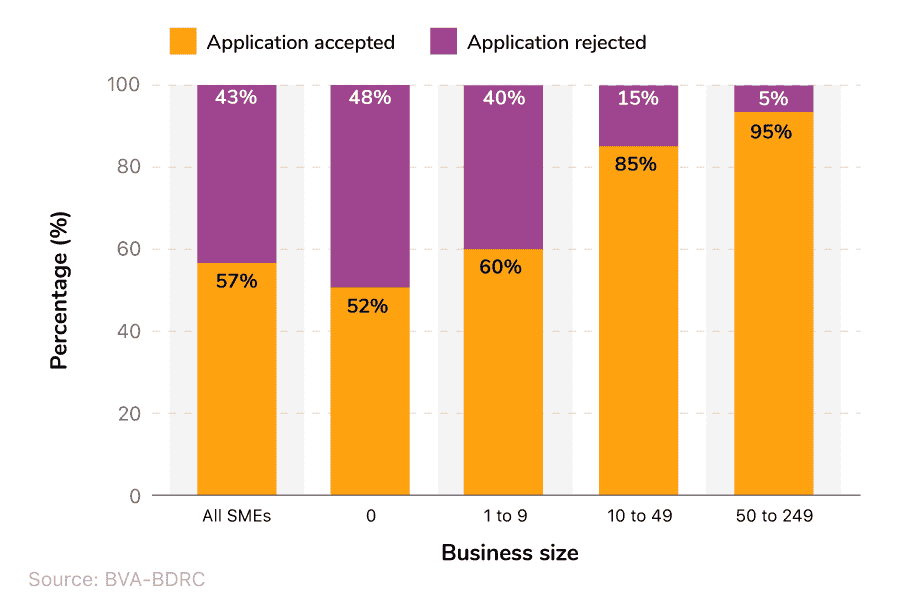

How many UK SMEs are approved for business loans?

At the time of writing, UK business lending statistics indicate that almost three-fifths of UK SMEs had their business loan application approved between Q3 2023 and Q4 2024.

The percentage of UK SMEs that had their external finance application accepted and rejected by business size

Data from BVA-BDRC’s SME Finance Monitor suggests that as a business increases in size (i.e., the number of employees), its chances of having its business loan application approved also increase.

For example, just over half of microbusinesses between Q3 2023 and Q4 2024 were successful in their business loan application, a figure that rises to:

Three in five companies with one to nine employees.

Almost six in seven corporations with 10 to 49 workers on their books.

19 in every 20 businesses with a workforce size between 50 and 249.

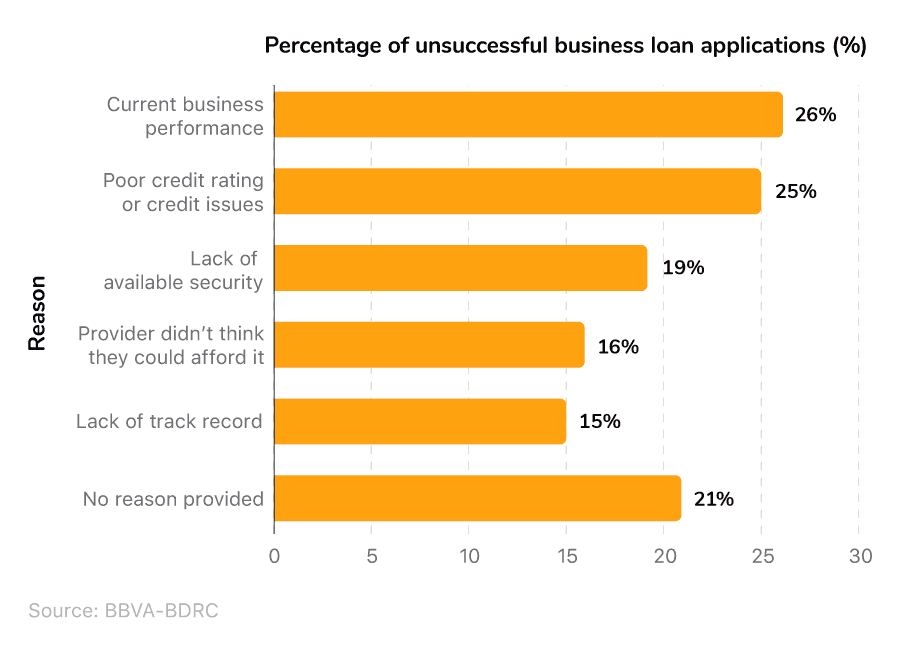

How hard is it to get a business loan?

The most common reasons for having a business loan application rejected are either poor current business performance or a poor credit rating with existing credit issues. These were each cited by around a quarter of businesses surveyed by the BVA BDRC in 2024.

Most common reasons for having a business loan application rejected

According to business lending statistics, around one in five UK companies have been rejected for a business loan due to a lack of available security, with a sixth claiming their provider didn’t think they could afford it.

Can you get a business loan with bad credit?

It’s possible to obtain a business loan with bad credit, but you may find the process takes longer and is more challenging compared to someone with a good credit history.

Businesses with a poor credit rating tend to have fewer lenders to choose from, as they’re perceived as high risk and less likely to be able to repay the borrowed money in the future. Therefore, you may need to consult a specialist lender with more flexible lending criteria.

Getting a start-up loan with a poor credit history can be equally as challenging, as lenders tend to view smaller businesses as a risky investment. You might also expect to pay above the average business loan interest rate and/or borrow a smaller amount to mitigate the risk from the lender’s perspective.

UK business start-up loan statistics

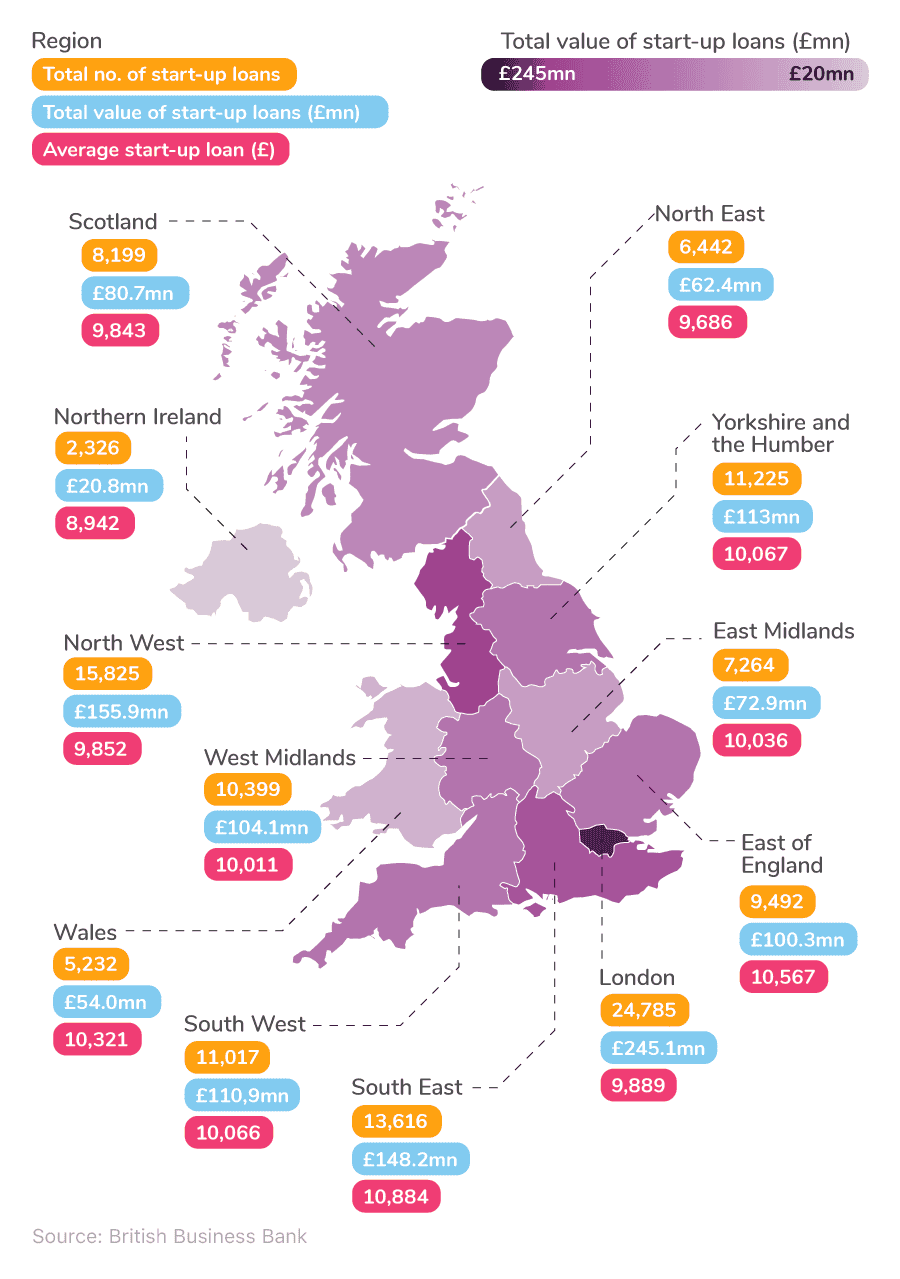

Since the beginning of the COVID-19 pandemic, the number of start-up loans taken out by aspiring UK entrepreneurs has increased by more than a fifth, reaching 120,221 as of December 2024.

During this time, the value of UK start-up loans has exceeded £1.19 billion (an increase of £176 million in the space of five years).

According to the latest UK business statistics, the average business loan for start-ups stood at just under £9,950 in December 2024. This represented a rise of almost a fifth (or £2,143) from 2020 figures.

Of these loans:

The number of people from an ethnic minority background increased by 5.39% between 2015 and 2020.

Around one in 10 were aged between 18 and 25, with one in eight aged 50 and above. This means more than a fifth came from these two age groups alone.

More than half (56%) of recipients were aged 31-49 years old and formed the majority of start-up loan approvals as of December 2024.

Which region borrows the most in start-up loans?

Newly launched businesses in the South East typically borrow the most, with the average start-up loan in this area standing at £10,884. The region’s overall value of start-up loans was just under £148.2 million as of December 2024. According to business lending statistics, this is the third-highest figure behind London and the North West.

Although London’s total loan value of £245.1 million is around two-thirds higher than the South East's, its average loan value of £9,889 is approximately 9.1% lower by comparison. This is because almost twice as many start-up loans are issued in London compared to the South East (24,785 vs 13,616).

Total number and value of UK start-up loans

Northern Ireland’s average start-up loan was the lowest of any UK region, at £8,942. This figure was 9.2% lower than that of the next lowest region (Scotland). Northern Ireland also recorded the lowest overall loan value, at approximately £20.8 million (almost 12 times less than start-ups receive in the capital).

Check out our guide on how to turn business ideas into a reality.

UK external finance statistics for businesses

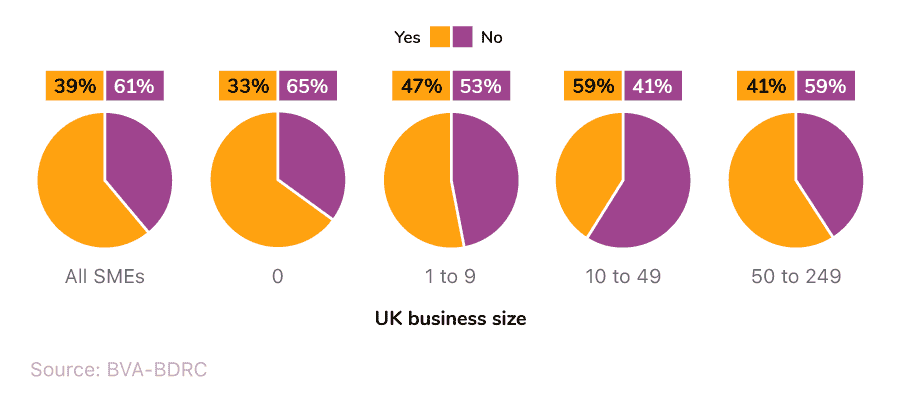

How many UK SMEs require external finance?

According to the latest business loan statistics from the BVA BDRC, two in five UK SMEs reported requiring external finance in 2024.

Use of traditional external finance by different-sized UK businesses

Generally speaking, as a company increases in size by the number of employees, so does the proportion who turn to traditional external finance.

For example, just over a third of microbusinesses (i.e., those with no employees) used traditional external finance in 2024, rising to almost three-fifths for those who employ between 10 and 49 people.

This figure reduced to around two in five for UK SMEs with 50 to 249 employees.

Examples of traditional external finance include business credit cards, bank overdrafts, bank loans, commercial mortgages, and any other form of loan/overdraft.

Use of any form of external finance by different-sized UK businesses over time

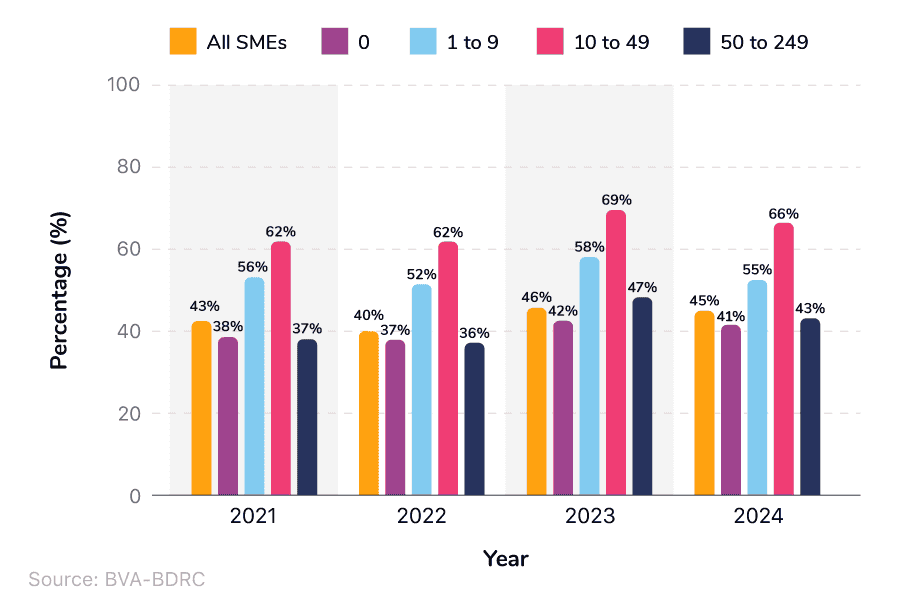

Since 2021, the proportion of SMEs turning to external finance has fluctuated between 40% and 46%, meaning less than half of the UK’s small and medium-sized corporations still rely on some level of external funds to keep their business going.

Since 2021, SMEs with between 10 and 49 employees have tended to borrow the most external finance across all SME sizes, rising to almost seven in ten in 2023 (the highest recorded figure in the past four years).

What are the most popular types of external finance for UK SMEs?

According to small business lending statistics from the BVA BDRC, the most common form of external finance used by UK SMEs in 2024 was credit cards, at around one in six cases. This was followed by more than one in 10 who opted for a bank overdraft.

Most common types of external finance used by UK SMEs

| Type of external finance | All SMEs | 0 | 1 to 9 | 10 to 49 | 50 to 249 |

|---|---|---|---|---|---|

| Credit cards | 15% | 13% | 18% | 32% | 23% |

| Bank overdraft | 11% | 10% | 14% | 18% | 16% |

| Bank loan | 9% | 8% | 14% | 19% | 14% |

| Commercial mortgage | 2% | 1% | 3% | 6% | 5% |

| Any other loan | 1% | 1% | 2% | 2% | 1% |

| Leasing or hire purchase | 10% | 7% | 14% | 30% | 21% |

| Loans from directors, family, and friends | 8% | 8% | 10% | 9% | 3% |

| Equity from directors, family, and friends | 2% | 2% | 4% | 3% | 1% |

| Invoice finance | 1% | 1% | 2% | 5% | 8% |

| Grants | 2% | 2% | 3% | 5% | 4% |

(Source: BVA BDRC)

Credit cards remain the most popular type of external finance for all types of SMEs, accounting for nearly a third of those with 10 to 49 employees. This is more than double the proportion among microbusinesses.

Data from the 2024 SME Finance Monitor also shows that companies with 10 to 49 workers tend to use external finance more than any other, with:

Three in 10 choose a leasing or hire purchase (four times more common than those employing zero people).

Almost one in five opting for a bank loan (double the proportion of microbusinesses).

A similar percentage relying on a bank overdraft (the highest figure across all-sized SMEs).

For more information, check out our guide on practical ways to get business finance.

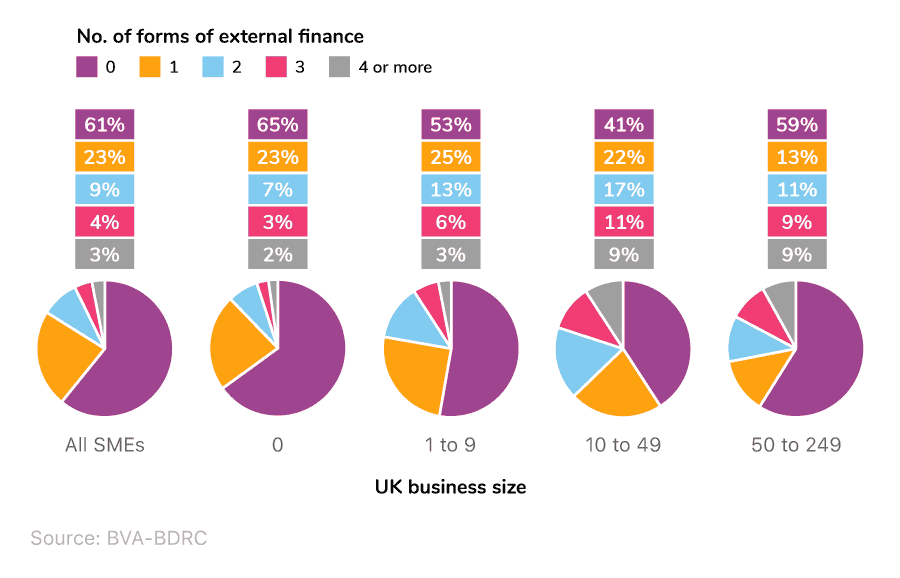

How many different forms of external finance are used by UK SMEs?

Almost a quarter of UK SMEs used one type of external finance in 2024, compared to three in five who opted for no external finance at all.

Number of forms of external finance used by UK SMEs

More than one in six companies with 10 to 49 employees chose at least two forms of external finance in 2024 (more than double the average UK SME), with around one in 10 taking out three. This was approximately three times more common than in most small and medium-sized businesses in the UK for the year.

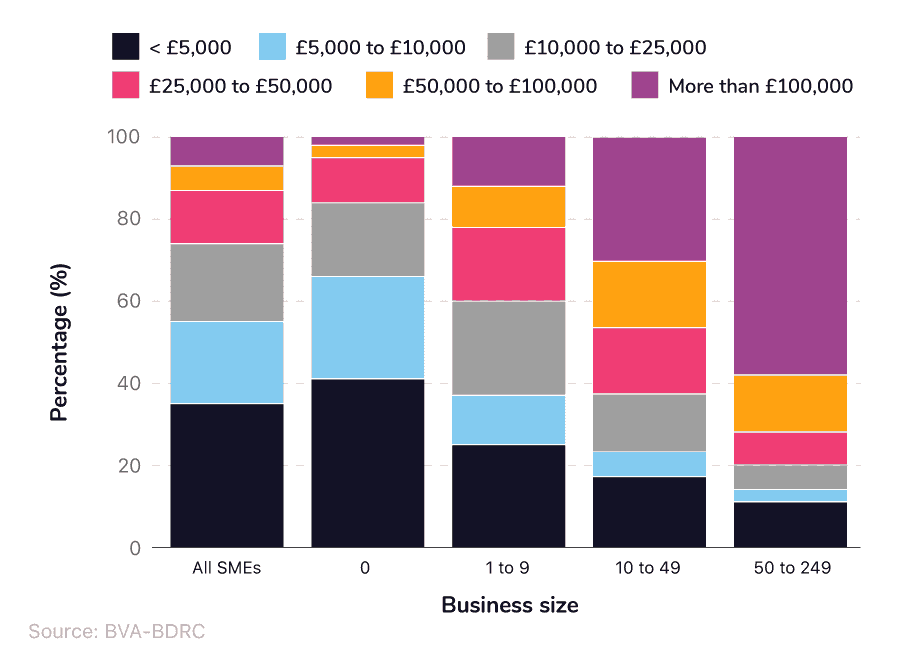

How much does the average SME borrow for external finance in the UK?

According to small business lending statistics from the BVA BDRC, more than a third of UK SMEs borrowed £5,000 or less in 2024.

Generally speaking, as the average amount of external finance increases, the proportion of SMEs borrowing that amount tends to decrease, with around one in 14 opting to borrow more than £100,000.

Average amount of external finance borrowed by UK SMEs

Larger SMEs tend to borrow more money than smaller ones, with almost three-fifths of companies with 50 to 249 employees choosing external finance above £100,000 in 2024, compared to around one in 50 microbusinesses.

Conversely, two in five microbusinesses borrowed less than £5,000 in 2024, which is around four times the proportion of those with 50 to 249 workers.

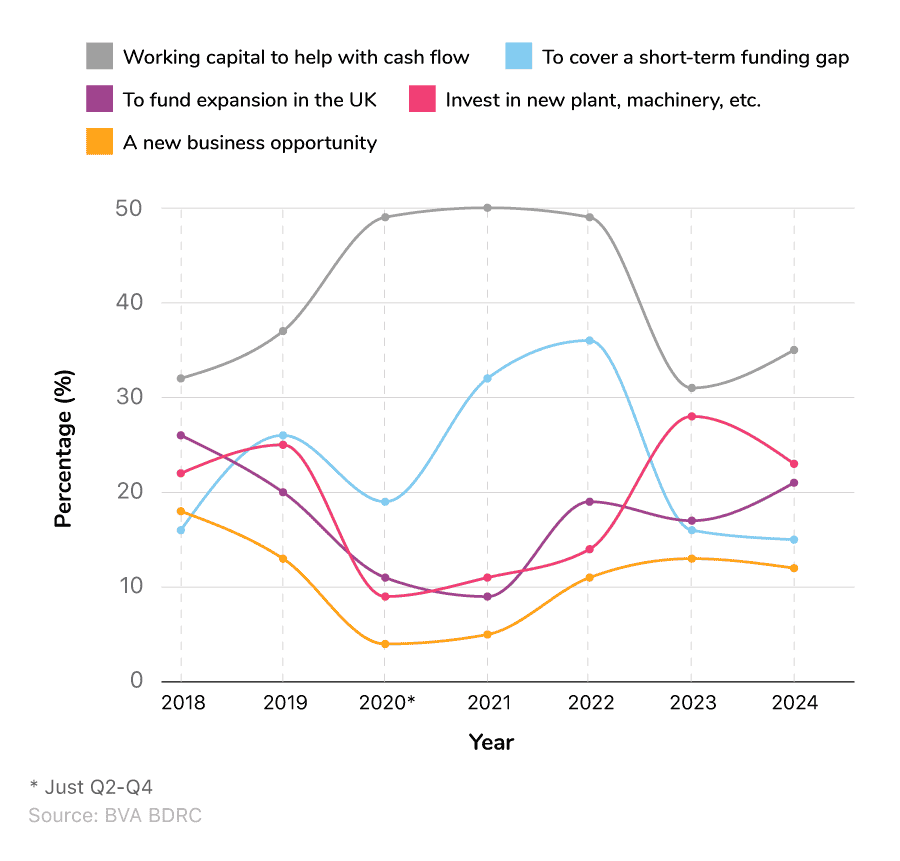

What are the most popular reasons for UK SMEs requiring external finance?

As of 2024, the most common reason UK SMEs require external finance is to provide working capital, helping with cash flow.

This was cited by more than a third of businesses surveyed by the BVA BDRC, representing a 15 percentage point decrease from a peak in 2021, when half of those questioned gave this as their primary reason for using external finance.

The most common reasons why UK SMEs require external finance over time

Almost a quarter of SMEs used external finance in 2024 as an investment opportunity for new equipment (a figure that has more than doubled since 2021).

That said, in 2022, more than one in three UK SMEs were using external finance to cover a short-term funding gap. However, by 2024, the proportion doing so had more than halved.

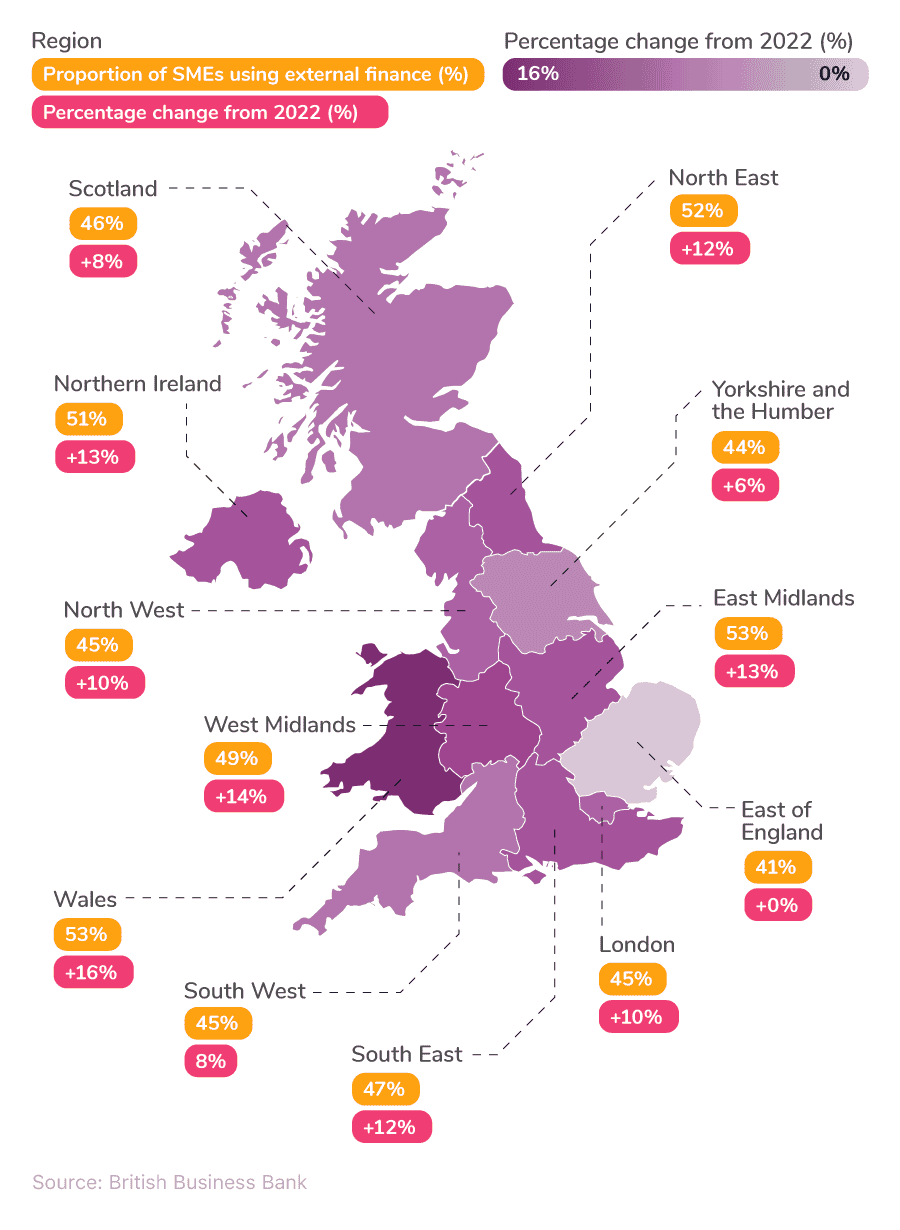

External finance statistics by region

Small business statistics from the British Business Bank show that more than half of SMEs in Wales, the North East, and Northern Ireland used some form of external finance in 2023; the highest proportion across all UK regions.

This was contrasted by around two in five SMEs from the East of England.

Proportion of UK SMEs using external finance across different regions

Wales saw the biggest percentage change from its 2022 figures, with numbers rising by a sixth in the space of 12 months.

Conversely, external finance lending statistics to SMEs in the East of England remained unchanged in 2023 compared to the previous year (the only UK region not to experience an increase in its reported figures during this period).

The future of external finance applications for UK SMEs

Almost one in five SMEs surveyed by the BVA BDRC in 2024 claimed that they intend to inject personal funds into their business at some point in the future. This figure is comparable mainly for UK microbusinesses, but this tends to decrease as the company size increases.

How likely are UK SMEs to apply for external finance in the future?

| Response | All SMEs | 0 | 1 to 9 | 10 to 49 | 50 to 249 |

|---|---|---|---|---|---|

| Need more external finance | 9% | 8% | 12% | 10% | 7% |

| Apply for more external finance | 8% | 7% | 10% | 10% | 6% |

| Renew existing borrowing at the same level | 4% | 2% | 7% | 5% | 3% |

| Reduce the amount of external finance | 12% | 11% | 16% | 13% | 6% |

| Inject personal funds into the business | 19% | 20% | 17% | 10% | 3% |

(Source: BVA BDRC)

Around one in eight UK SMEs believe they will reduce the amount of external finance they borrow in the future (a figure that rises to one in six of those with one to nine employees).

Less than a tenth of SMEs believed they would require additional external finance in the future and would apply for it accordingly.

Unsure whether to seek external finance? Our comprehensive guide will help you decide whether borrowing could boost your business.

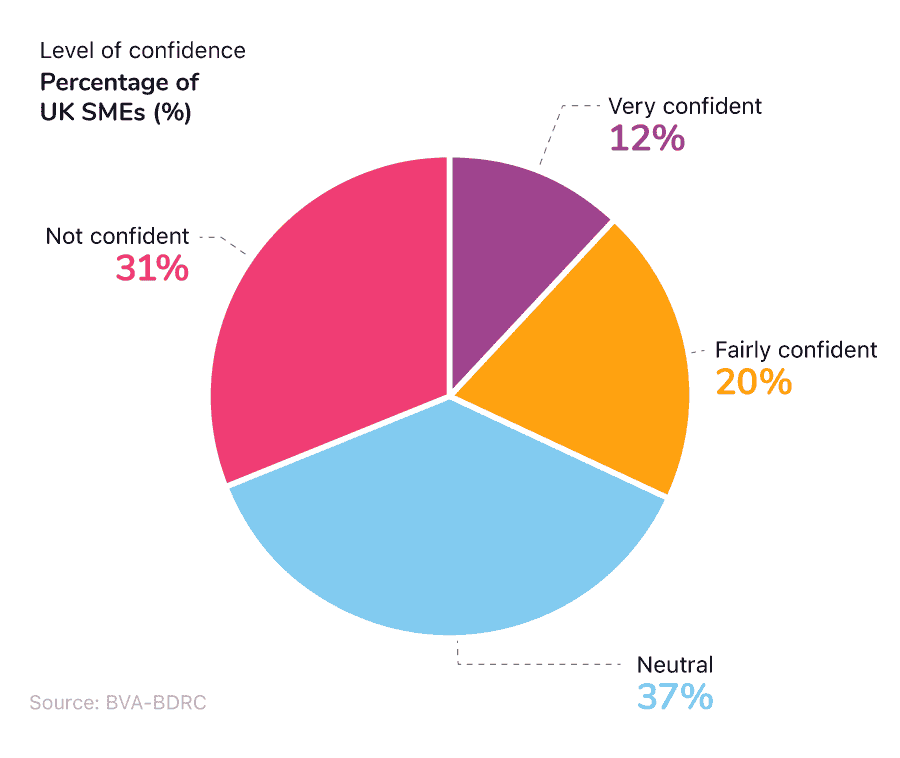

How confident are UK SMEs that they will get external finance in the future?

The latest small business lending report from the BVA BDRC found a fairly even split between SMEs in terms of how confident they feel about getting external finance in the future.

Just under a third felt they would be given the money they require, with an almost identical percentage not convinced that they would.

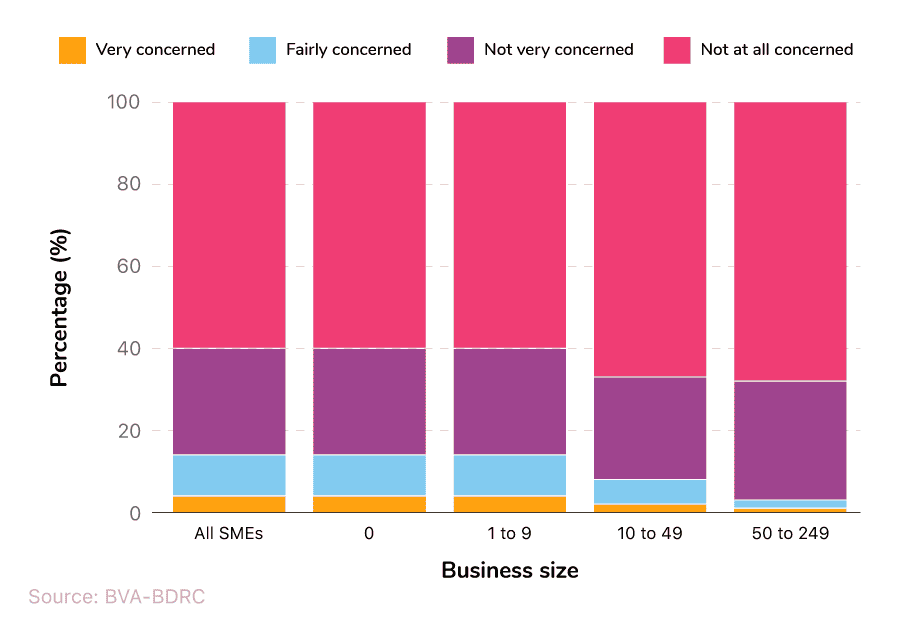

How concerned are SMEs about repaying external finance?

Three-fifths of SMEs questioned by the BVA BDRC said they were not concerned about repaying any external finance they had borrowed. This figure rose to more than three-quarters for larger SMEs, particularly those employing more than 10 people.

Generally speaking, levels of concern remain relatively low amongst the SME population, with less than one in six expressing that they’re very or fairly concerned about repaying their external finance in the future.

Smaller businesses tend to be more worried about this than larger corporations, with 14% of microbusinesses claiming to be very or fairly concerned compared to 3% of those with 50 to 249 employees.

Want advice on how to get a business loan? Visit our comprehensive business loans guides for expert tips on this and more.

Business loans FAQs

What is a secured business loan?

A secured business loan is a type of business loan that allows you to borrow money against the value of an asset as collateral, providing security. This lowers the risk of lending, resulting in lower interest rates compared to an unsecured loan. It also opens up the possibility of borrowing a greater sum of money.

What is an unsecured business loan?

An unsecured business loan is a type of business loan that assesses the finances of your business to determine the likelihood that you’ll be able to repay the money when required.

What is a small business loan?

A small business loan is a lump sum payment or a flexible line of credit designed to help entrepreneurs start or expand their business operations.

Can I get a business loan?

Yes, most people can get a business loan. However, you’ll need to meet the criteria set out by your lender before an application is approved.

Many lenders offer an eligibility checker before you submit a business loan application. This will give you an idea of how likely you are to obtain a business loan and identify any potential issues before you undertake a formal credit check.

How hard is it to get a loan to buy a business?

It can be challenging to get a loan to buy a business. According to business loan statistics from the BVA BDRC, around two in five UK SMEs had their business loan application rejected in 2024. The most commonly cited reason for this was the current performance of the business (26% of cases).

How to get a business loan

To get a business loan, there are several steps you should take to make your application as successful as possible.

Have a business plan in place; this will provide the lender with a clear vision of your business model and how you intend to repay the loan.

Calculate how much you need to borrow - this should be enough to support the growth of your company and reduce the likelihood of having to borrow more in the future.

Consider how long you need the loan for - choosing a longer term can reduce your monthly repayments, but could mean paying more in interest.

Check your business credit score - this may influence your chances of approval (i.e. those with a better score are likely to be granted the amount of money they want to borrow).

Get your finances in order by settling any outstanding debts, as this can improve your credit rating ahead of your business loan application.

Before agreeing to a business loan, it’s essential to make sure you can comfortably repay the money borrowed without damaging the success of your business. Consulting an independent advisor is a step in the right direction to help you make a decision that is right for you and your company.

How does a business loan work?

A business loan is obtained by applying to a lender. They will consider the financial stability of your business, how creditworthy a loan would be to its success, and the likelihood that you will repay the borrowed money in the future.

Once approved, the lender will transfer the agreed-upon amount as a lump sum to your business bank account, allowing you to start investing.

How much of a business loan can I get?

How much of a business loan you can get will depend on several factors, such as the type of loan you’re after, your business’s credit history, and what your lender feels you can realistically pay back.

Depending on the above, the amount of borrowing for an unsecured loan could be as much as £750,000, while for a secured loan, it could be up to £15 million. Alternatively, for those getting their business off the ground, you could borrow up to £25,000 from a government-backed Start Up Loan.

What is the average business loan amount in the UK?

Around three-fifths of UK SMEs borrow up to £24,999 when it comes to taking out a business loan.

What are business loan interest rates?

Business loan interest rates refer to the additional sum of money that must be repaid, in addition to the initial amount borrowed, when you took out the loan.

For example, if you borrowed £100,000 over three years at an agreed interest rate of 9%, your total repayment would be £114,479, making the cost of the loan (excluding any fees) £14,479.

What is the average business loan interest rate in the UK?

As of June 2025, the average business loan interest rate in the UK stood at:

6.17% for Private Non-Financial Corporations (PNFCs), and 5.96% for SMEs on the stock of outstanding loans.

5.94% for new loans to PNFCs and 6.51% for new loans to SMEs.

How big is the business loans market in the UK?

The UK business loans market was worth a reported £485.9 billion as of 2024, a 1.3% decrease from the previous year.

What is the value of SME lending in the UK?

The total value of SME lending in 2024 stood at £62.1 billion (a 4.9% increase from 2023).

Business loans glossary

Glossary of terms

Asset-based lending

Asset-based lending is when a business uses an asset, such as a building, premises or inventory, as collateral in order to acquire finance.

Government grant

A government grant is a sum of money awarded to your business by the UK government. You do not have to pay back these sums. Grants are typically awarded to companies to fund specific developments.

Gross lending

Gross lending refers to the total amount of loans a bank or institution advances over a given period. It excludes repayments and other adjustments.

Hire purchase

Hire purchase is where a business or individual acquires an item without paying the full purchase price at the outset. Instead, they make pre-arranged payments according to an established schedule.

Invoice finance

Invoice finance is when a business uses unpaid customer invoices as collateral to acquire funding from a lender.

Overdrafts

An overdraft is a form of debt that allows you to take out more money than you have in your bank account. You are said to be overdrawn if your balance falls below £0. There is generally a limit to your overdraft and a charge for being overdrawn.

Start-up loans

Start-up loans are supplied as part of a government-backed scheme in which prospective new businesses (or businesses that have been trading for less than 36 months) can receive funding to help with costs like equipment, stock, premises, marketing and promotional expenses.

Sources

https://www.ibisworld.com/united-kingdom/bed/business-lending/44246/

https://www.bankofengland.co.uk/statistics/visual-summaries/businesses-finance-raised

https://www.bankofengland.co.uk/explainers/current-interest-rate

https://www.bankofengland.co.uk/statistics/visual-summaries/effective-interest-rates

https://www.bva-bdrc.com/wp-content/uploads/2025/03/SME-FM-FULL-REPORT.pdf

https://www.ukfinance.org.uk/data-and-research/data/sme-lending-within-uk-postcodes

About Cameron Jaques

Cameron has worked within the SME industry for over five years, looking after all our SME commercial relations for money.co.uk including business loans, business current accounts, and business credit cards.